It’s natural to have accounting questions when starting and running a business, but accounting can be a daunting subject (and sometimes more than a little dry). To help get you comfortable, we’ve answered a few of the most basic questions that are likely to come up as you start and grow your small business.

Basic Accounting for Small Business

Subjects like increasing revenue and marketing tend to be the flashier steps of starting a small business, but the back-end stuff like accounting can’t be overlooked. Accounting will tell you the bottom line—how profitable are you? If you think of it in those terms, it’s surprising that more people don’t LOVE accounting.

Love it or hate it—accounting is critical, and luckily you don’t have to go get your degree in accounting to successfully grow. But you DO need to understand some key components of the practice to ensure you’re making the best decisions for your business, namely:

- What exactly IS accounting?

- What options do you have for accounting services?

- What do you need to know before setting up your accounting?

Understanding these questions is key to starting your small business accounting system off on the right foot, so we’ll cover all three.

What is Accounting?

Simply put, accounting is the function of organizing the financial data in your business. You earn revenue, you incur costs, you pay employees—how do you account for that? Specifically, how do you record these transactions for your business? All accounting entries (called journal entries) must consist of the following data points:

- A date

- An account to be debited or credited (does the account go up or down)

- The amount to be debited or credited (does the account go up or down)

- A brief description

- A unique reference number

Here’s a sample of a journal entry, courtesy FundsNet:

We just tossed out some accounting lingo, but since the goal of this is to understand the basics, we’ll abstain from going into detail regarding debits and credits. Suffice to say, you need to indicate whether money is flowing in or out of the account. For more help translating accounting language, check out our handy list of basic accounting terms.

What is an Account?

Accountants use accounts to keep business numbers organized. Think of them like buckets within your business—all of the money that flows through your business needs to be categorized somehow—that’s what accounts are used for.

For example, let’s say you invested money in your business, this would be tracked in the Owners’ Equity account.

Or if you earned revenue from sales, this would be tracked in your Sales account.

Does your business keep inventory on hand? If so, you would record this in your Inventory account.

These are just a few examples of the different types of accounts, but you get the picture. In essence, the flow of money in your business is recorded, tracked, and monitored by your Accounting.

If you’re wondering why this is all so important, it really comes down to having the ability to share your “books” with someone else in order for them to assist you with your business. You’ll need to share your books in cases like:

- Filing taxes

- Applying for a business loan

- Raising investment from angel investors or VCs

- Selling your business

- M & A

While these are the reasons you would want to share your books with someone, the most valid argument for proper accounting is that it provides guidance to you—the owner and executive team—for growing your business.

Through proper analysis, accounting shows you where you are crushing it as well as where you’re struggling. Are you running out of cash? Do you have more expenses than your competition? Is your profit margin lower than planned? Accounting provides the framework for this type of analysis—without it, these questions would remain unanswered.

57 Sales Tips That Actually Work!

From the President of PaySimple to You: The Small Business Sales Guide

Click here to access the FREE guide

What Options Do You Have for Accounting Services?

Next up, as a business owner you should be aware of the various accounting options available to you. In brief, they are:

- Track it yourself (either using a cloud software like Quickbooks Online or by tracking transactions in an Excel spreadsheet)

- Outsource your accounting

- Hire an in-house accountant

Depending on the size of your business and the number of transactions you have, one of these options will likely stand out as your preferred pick. Let’s break those down with a bit more color around the pros and cons of each option.

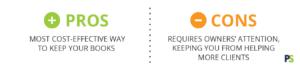

Track your small business accounting yourself

Keeping track of your own accounting is the preferred option for many businesses in the start-up stage, as well as many lifestyle businesses. If you operate a one or two-person service-based business, this may be the best option for you (i.e., lawyer, therapist, plumber, etc.).

Generally, these types of businesses are a bit smaller and tend to have a manageable number of transactions. In these cases, business owners will often monitor revenue and expenses through Excel spreadsheets or Quickbooks Online. Quickbooks Online, or QBO as it is often referred, is widely considered the gold standard of small business accounting systems.

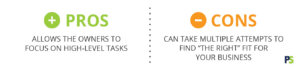

Outsource your small business accounting

Today, there are many options for businesses looking to outsource their accounting. Making this choice can be beneficial for a business with owners who are poised to grow the company as it allows them to delegate this task to a professional bookkeeper or accountant while they focus their energies elsewhere. Popular options can be generally boiled down into three buckets:

- Low cost leaders (think Bench.co)

- Mid-range services (local bookkeepers)

- High-end services (CPAs and the like)

Outsourcing your accounting can be tricky since it’s hard to know what you’re getting until you’ve paid for the service. While the low cost leaders might be more appealing to your wallet, bear in mind that they often cannot offer many services. For example, Bench currently doesn’t offer help with 1099s or renewing business licenses. They also don’t have a built-in payroll option.

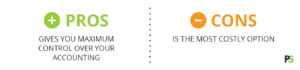

Hire an in-house accountant for your small business

In-house accountants or bookkeepers are definitely the most costly option, but once your business has grown to certain point, this becomes your best option.

Unfortunately, it’s difficult to say when you’ve outgrown an outsourced accountant, but most of the time, your monthly charges will be a good indication. If you are watching your outsourced accounting bill go up and up, do the math to determine if it’s in your best interest to bring this role in-house.

How are you accepting payments?

Learn all the ways to accept online payments

Click here to access the FREE [Cheat-Sheet]

The average bookkeeper salary is currently around $45,000 per year, +/- $5,000. If your accounting fees are nearing this amount, it’s probably time to make it an in-house position. Of course, there is a difference between bookkeeping and accounting. If your accounting needs are more complex, then an accountant may be your preferred option (and naturally, they come with a higher salary requirement).

As in all things, you get what you pay for with accounting. If your needs are more complex (and they will be, as your business grows) then the more expensive options are going to be preferable to you due to the insights and level of control you’ll receive.

What Do You NEED to Know Before Setting Up Your Accounting?

By now, you have a decent idea of what accounting IS for small businesses as well as what options exist for setting up accounting for your small business. Lastly, let’s cover the biggest question you’ll face when setting up your accounting: should you use the CASH or ACCRUAL basis?

Accounting has to follow rules known as Generally Accepted Accounting Principles (GAAP). These rules ensure that everyone performs accounting in the same manner.

GAAP permits that you can use either the cash basis or the accrual basis when you account for your business. It also dictates that you must continue using one basis consistently, although you can elect to change your accounting basis, but it requires filing forms with the IRS to do so.

Cash vs. Accrual—How Does the Decision Affect Your Business?

Remember the five elements of a journal entry? The first of these is “a date.” That is, every transaction you record has to have a date associated with it. What date you use to record your transactions is entirely dependent upon whether you elect to report on a cash basis or an accrual basis.

To make this easier to understand, imagine you performed your service on February 1, sent an invoice on February 3, and received the payment on March 2.

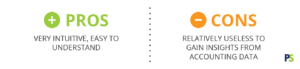

Cash Basis:

The Cash basis uses the date that the cash is either received (revenue) or paid (expenses). In the above example, we would record a journal entry with a date of March 2, because that is the date that the payment was received.

Accrual Basis:

The Accrual basis uses the date that the revenue was earned or the expense was incurred. So, in our example, we would record a journal entry with a date of February 1, since this is the date that we performed the service.

This was a simple (one-transaction) example, but you can imagine how this difference would be compounded in a business with a heavy number of transactions. Many owners start on a cash basis but eventually switch to an accrual basis once the business has become more complex. Regardless of which option you choose, make sure that you understand what the rules of your reporting are. Without that understanding, you won’t be able to tell if your business is doing well or if there’s trouble afoot—and in that case, what are you accounting for in the first place?

Start a 14 day Free Trial and streamline your business with PaySimple: